Implementation

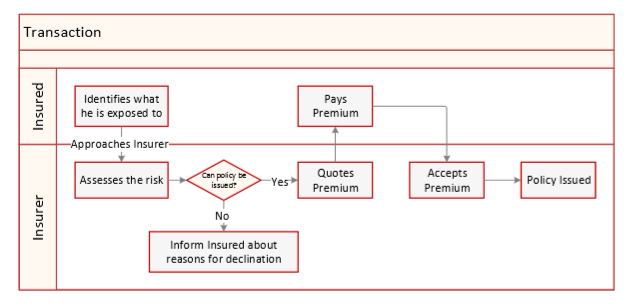

What is a Transaction?

In simple words, it is just an exchange, where an individual gives something in return for something.

In the case of Insurance, it is a transfer of risk, where an individual pays premium (consideration) to an Insurance Company to protect himself from loss.

Types of Transactions

Different types of transactions can be processed on an Insurance Contract (Policy) during the Policy Term (Policy Effectivity).

❖ New Business

❖ Endorsement

❖ Cancellation

❖ Reinstatement

❖ Renewal

❖ Re-issue

❖ Re-write

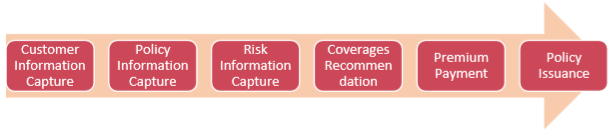

New Business

A policy that is issued for the first time to a Customer is called New Business. As part of New Business, the Insurance Company needs to understand the Customer, their risks, provide them with the right coverages and finally issue a policy. Therefore, New Business is all about offering quotes and issuing a policy after customer acceptance.

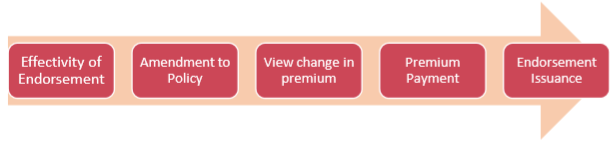

Endorsement

Endorsement is a transaction through which an Insured can request for amendment in his policy information. As part of Endorsement, an Insured can opt for more coverages, add / delete specific risk information, and make any desired change to the Policy. The Insurer will assess the changes made and charge additional premium or refund some part of the premium paid during New Business (as the case may be).

Cancellation

Cancellation is a transaction through which an Insured can cancel his policy and request for a refund. In certain cases, the Insurer also initiates cancellation. After Cancellation, the policy stands cancelled, and Insurer processes a refund to the Insured (if any).

Types of Cancellation – Pro Rate, Short Rate and Flat Rate.

Pro Rata Cancellation

A pro rata cancellation is a full refund of any unearned premiums. This amount is proportional to the amount of time remaining on the policy.

For example, if an insured pays a premium of $12,000 for the year, but the policy is cancelled after 6 months on a pro-rata basis, the insurer returns $6000 to the insured—50% of the policy remaining means 50% of the premium is refunded.

Pro rata cancellations are applied when the insurer cancels the policy. This usually happens because of some material change in circumstances and the insurer does not feel comfortable staying on the policy.

Short Rate Cancellation

A short rate cancellation is the same as a pro rata refund minus some administrative costs or minimum retained premium. Short rate cancellation is a financial penalty incurred when the insured cancels an insurance contract prior to the expiration date of the contract. This allows the insurer to keep a percentage of unearned premium to cover various administrative costs.

Flat Rate Cancellation

To flat cancel an insurance contract means to cancel the insurance contract before that contract's effective date. The timing is significant because it means that the insuring company has not assumed any liability under the contract, since the contract has not begun. As such, the insured (customer) is entitled to a full refund of any premiums paid without any deductions of any kind.

While this is in no way, a standard procedure; sometimes dispute between an insured and the insurer that resulted in both parties settling via a flat cancellation of the policy. However, this is not a typical case and there were most likely extenuating circumstances that lead to this type of resolution.

Reinstatement

Reinstatement is a transaction through which an Insured can request the Insurer to bring his cancelled policy back in-force. After Reinstatement, the policy that was cancelled earlier, again becomes a valid contract. This means the Insured continues to remain covered by paying the premium again.

Types of Reinstatement – Regular Reinstatement, Reinstatement with Lapse.

Reinstatement without lapse:

Regular Reinstatement is when the policy is brought back into activation immediately after the expiration of policy and thereby, reinstatement considers the same effective date which is the starting date of the policy. The policy continues to be in activation as though the lapse never occurred.

Reinstatement with lapse:

In this type of reinstatement, the policy stays in place and comes with new effective dates according to when the insured (customer), would want to bring the expired policy into activation. If any unplanned event occurs while policy is lapsed, the insurance company would not cover any claims during the lapse period.

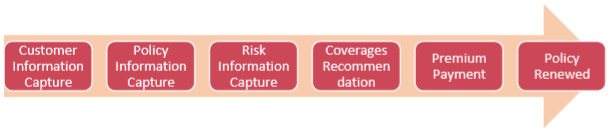

Renewal

After the expiry of a policy term, through Renewal transaction, the Insured can choose to continue to remain covered for another term. The process of a Renewal is like New Business. As part of Renewal, the Insured can make amendments to his policy information if needed and pay premium to remain covered.

Re-issue

When an Insured wants to correct non-premium bearing information after the policy is issued, he can request the Insurer to reissue the policy.

When the Insured opts for reissuance, a quote is created, and the policy information is copied onto the quote. The changes can be made, and the policy will be issued with the same policy number. Basically, the same policy is modified.

Re-write

Sometimes a policy is issued with errors in risk structure due to misinterpretation of information. A rewrite transaction can be processed to correct such errors.

When the Insured opts for rewrite, a quote is created, and the policy information is copied onto the quote. The changes can be made, and the policy will be issued with a different policy number. The older policy is flat cancelled as soon as a quote is created during rewrite.

Policy ProRate Factor

ProRate Factor for the policy is calculated based on the effective date and the expiry date of the policy. The difference in the effective date and expiry date by total number of days in the policy is termed as effective period of the policy.

Coverage ProRate Factor

When one or more than one coverage under a risk is prorated with a factor to hold back the proportion of premium in case of early cancellations, regardless of the policy period; such coverages are termed to be partially earned coverages.